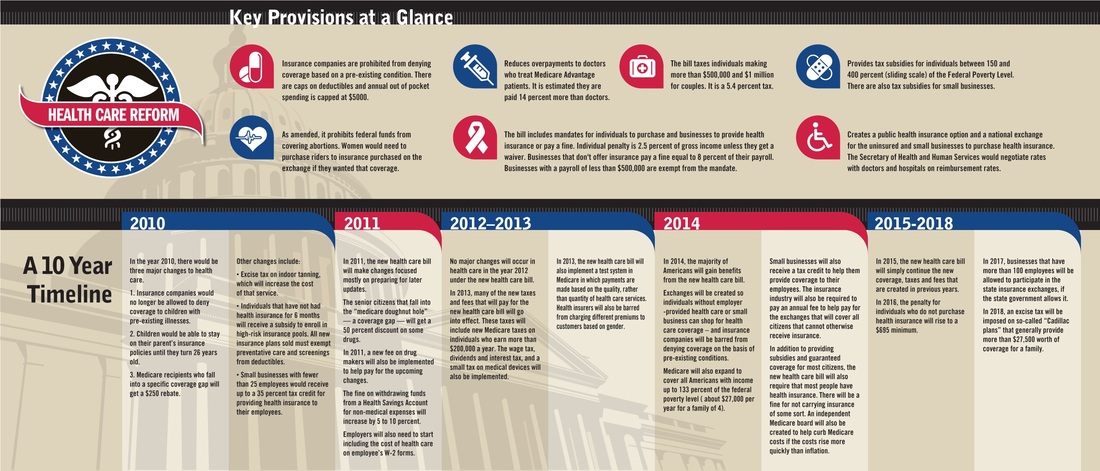

Health Care Reform Information

CLICK IMAGE TO ENLARGE

After a year of debate, Congress passed health care reform legislation, although the complete legislation is not yet finalized. On March 21, 2010, the House of Representatives passed the Senate-version legislation, the Patient Protection and Affordable Care Act (H.R. 3590) (the "Affordable Care Act").

Numerous state legislators are already passing laws to exempt their citizens from elements of the health care reform package, specifically the individual and employer mandates. Whether these laws are preempted by federal legislation will be an issue for the courts to address.

As the health reform legislation stands today, the issues affecting individuals and employers are outlined below in order of implementation deadline.

The US Department of Health and Human Services has launched a very helpful web site with a tremendous amount of information on the new Affordable Care Act.

One of the greatest features of their site is the Timeline page. It allows you to understand what is changing and when at the click of your mouse! This interactive page will make learning about the changes ahead easy for you and your family.

For any information you cannot find online, please don't hesitate to contact us! We are very knowledgeable on the new Affordable Care Act and looks forward to helping you understand it, too.

90 DAYS AFTER ENACTMENT

Temporary Retiree Reinsurance Program

Ninety days after enactment, a federal reinsurance program will be available for employers providing insurance for retirees over age 50 years of age, who are not eligible for Medicare. The program will reimburse employers for 80 percent of claims incurred for the retirees between $15,000 up to $90,000.

National High-Risk Pool

Ninety days after enactment, a federally subsidized high-risk pool will be established for individuals with preexisting conditions who have been uninsured for at least six months. There are certain restrictions for variance of premiums according to age and a maximum cost sharing of $5950 for individuals and $11,900 for families. The legislation appropriates $5 billion for this high-risk pool.

SIX MONTHS AFTER ENACTMENT

Dependent Coverage

For plan years beginning six months after the date of enactment, grandfathered plans would be required to provide coverage for adult children up to age 26, if the adult child is not eligible to enroll in an employer-sponsored plan. The employer contributions for adult child coverage would still be included in gross income, unless the adult child qualifies as a federal income tax dependent.

No Rescissions

For plan years beginning six months after the date of enactment, grandfathered plans would be prohibited from rescinding coverage except in the case of fraud.

No Lifetime/Restrictive Annual Limits

For plan years beginning six months after the date of enactment, existing plans are prohibited from having lifetime limits on coverage or restrictive annual limits (as determined by the Health and Human Services Secretary).

Pre-Existing Conditions

For plan years beginning six months after the date of enactment, there can be no pre-existing limitation for coverage of children under age 19, however insurers could still reject those children outright for coverage in the individual market until 2014.

YEAR 2010

Small Employer Tax Credit

For years 2010 through 2013, businesses with fewer than 25 employees and average wages of less than $50,000 are eligible for a tax credit of up to 35 percent of the employer's contribution toward the employee's health insurance premium if the employer contributes at least 50 percent of the total premium cost or 50 percent of a benchmark premium.

Reporting on Medical Loss Ratio

Effective in 2010, health insurance plans are required to report the proportion of premium dollars spent on clinical services, quality, and other costs.

Medicare Prescription Drugs

The approximately 4 million Medicare beneficiaries who hit the so-called "doughnut hole" in the program's drug plan will get a $250 rebate in 2010. Next year, their cost of drugs in the coverage gap will go down by 50 percent. In 2011, the bill would also begin phasing down the beneficiary coinsurance amount in the coverage gap so that it reaches the standard 25 percent beneficiary coinsurance by 2020. Preventive care, such as some types of cancer screening, will be free of co-payments or deductibles starting this year.

YEAR 2011

Medical Loss Ratio

Effective in 2011, insurers must provide rebates to consumers for the amount of the premium spent on clinical services and quality that is less than 85 percent for plans in the large group market and 80 percent for plans in the individual and small group markets. A process will be established for reviewing increases in health plan premiums and requiring plans to justify increases. States are required to report on trends in premium increases and recommend whether certain plan should be excluded from the Exchange based on unjustified premium increases.

Medicare Advantage Plans

The Reconciliation Act would freeze Medicare Advantage (MA) payments for 2011. MA payments would be restructured by tying them to 100 percent of Medicare fee-for-service costs, providing bonuses for quality and making adjustments for unjustified coding patterns. The government currently pays the private plans an average of 14 percent more than traditional Medicare. Besides reducing payments overall, there will be a shift in funding, with some high-cost areas to be paid 5 percent below traditional Medicare and some low-cost areas to be paid 15 percent more than traditional Medicare.

YEAR 2013

Increase Tax for High-Income Taxpayers

Effective 2013, for single taxpayers with adjusted gross income (''AGI'') of $200,000 or more and joint filers with AGI of $250,000 or more, the Reconciliation Act would add a 3.8 percent tax on investment income from interest, dividends, annuities, royalties, rents and capital gains ("net gain from disposition of property"). The tax would not include income that is derived in the ordinary course of a trade or business that is not a passive activity. This 3.8 percent tax is in addition to the 0.9 percentage point increase in the Medicare payroll tax on earned income that is in H.R. 3590. This additional tax would not apply to qualified plan distributions under Code sections 401(a), 403(a), 403(b), 408 408A, or 457(b).

Flexible Spending Arrangements (FSAs)

The Reconciliation Act would delay the effective date of the new annual limit on health flexible spending arrangements until 2013, at which time the FSA contribution would be capped at a maximum of $2500, indexed thereafter to general inflation.

YEAR 2014

Insurance Reforms

In 2014, the Reconciliation Act would prohibit pre-existing condition exclusions (for children, the exclusions are prohibited starting six months after enactment) and annual limits on coverage (which were restricted beginning six months after enactment).

Employer Mandate

Effective in 2014, employers with more than 50 employees that do not offer coverage and have at least one fulltime employee who receives a premium tax credit will be fined an amount equal to $2,000 per full-time employee, excluding the first 30 employees from the assessment. Employers with more than 50 employees that do offer coverage but have at least one full-time employee receiving a premium tax credit because coverage is "unaffordable," will pay the lesser of $3,000 for each employee receiving a premium credit or $750 for each fulltime employee. Coverage would be considered "unaffordable" if the premiums for the class of coverage selected by the employee exceed 9.5 percent of family income (down from 9.8 percent in H.R. 3590). Employers with 50 or fewer employees are exempt from penalties.

Employer Voucher

Effective in 2014, employers that offer coverage would be required to provide a free choice voucher to employees with incomes less than 400 percent FPL whose share of the premium exceeds 8 percent but is less than 9.8 percent of their income and who choose to enroll in a plan in the Health Insurance Exchange. The voucher amount is equal to what the employer would have paid to provide coverage to the employee under the employer's plan and will be used to offset the premium costs for the plan in which the employee is enrolled. Employers providing free choice vouchers will not be subject to penalties for employees who receive premium credits in the Exchange.

Auto-Enrollment

Employers with more than 200 employees must automatically enroll employees in coverage offered by the employer. Employees may opt out of coverage.

Small Business Tax Credit

Small employers with no more than 25 employees and average annual wages of less than $40,000 that purchase health insurance for employees are provided with a tax credit. For 2014 and later, for eligible small businesses that purchase coverage through the Health Insurance Exchange, a tax credit is provided of up to 50 percent of the employer's contribution toward the employee's health insurance premium if the employer contributes at least 50 percent of the total premium cost. The credit will be available for two years. The full credit will be available to employers with 10 or fewer employees and average annual wages of less than $25,000.

Individual Mandate

Citizens and legal residents are required to have "qualifying health coverage" by year 2014. Those without coverage pay a tax penalty of the greater of $695 per year up to a maximum of three times that amount ($2,085) per family or 2.5 percent of household income. The penalty will be phased-in according to the following schedule: $95 in 2014, $325 in 2015, and $695 in 2016 for the flat fee or 1.0 percent of taxable income in 2014,2.0 percent of taxable income in 2015, and 2.5 percent of taxable income in 2016. After 2016, the penalty will be increased annually by the cost-of-living adjustment. Exemptions will be granted for those for whom the lowest cost plan option exceeds 8 percent of an individual's income, and those with incomes below the tax filing threshold (in 2009 the threshold for taxpayers under age 65 was $9,350 for singles and $18,700 for couples).

Individual Subsidies

Premium credits are made available to eligible individuals and families with incomes between 133 and 400 percent of the federal poverty level to purchase insurance through the Health Insurance Exchanges. The premium credits will be tied to the second lowest cost plan in the area and will be set on a sliding scale.

Benefit Design

Effective in 2014, an essential health benefits package is established that provides a comprehensive set of services, covers at least 60 percent of the actuarial value of the covered benefits, limits annual cost-sharing to the current law HSA limits ($5,950/individual and $11,900/family in 2010), and is not more extensive than the typical employer plan. Abortion coverage is prohibited from being required as part of the essential health benefits package. Effective in 2014, all qualified health benefits plans, including those offered through the Health Insurance Exchanges and those offered in the individual and small group markets (except grandfathered plans) are required to offer at least an essential health benefits package.

Expanded Medicaid Eligibility

States will have the option starting in 2014 to expand Medicaid eligibility to nonelderly, non-pregnant individuals who are not otherwise eligible for Medicare, with incomes up to 133 percent of the federal poverty level (FPL). From 2014 through 2016, the federal government will pay 100 percent of the cost of covering newly eligible individuals.

Health Insurance Exchanges

Effective in 2014, state-based Health Insurance Exchanges and Small Business Health Options Program (SHOP) Exchanges must be established, administered by a governmental agency or non-profit organization, through which individuals and small businesses with up to 100 employees can purchase qualified coverage. States are permitted to allow businesses with more than 100 employees to purchase coverage in the SHOP Exchange beginning in 2017. States may form regional Exchanges or allow more than one Exchange to operate in a state as long as each Exchange serves a distinct geographic area. (Funding available to states to establish Exchanges within one year of enactment and until January 1,2015).

YEAR 2018

Tax on Cadillac Plans

The Reconciliation Act delayed implementation of the tax on Cadillac Plans and increased the threshold above which the tax applies. Effective in 2018, an excise tax is imposed on insurers of employer-sponsored health plans with aggregate values that exceed $10,200 for individual coverage and $27,500 for family coverage. The tax is equal to 40 percent of the value of the plan that exceeds the threshold amounts and is imposed on the issuer of the health insurance policy, which in the case of a self-insured plan is the plan administrator or, in some cases, the employer. The aggregate value of the health insurance plan includes reimbursements under a flexible spending account for medical expenses (health FSA) or health reimbursement arrangement (HRA), employer contributions to a health savings account (HSA), and coverage for supplementary health insurance coverage, excluding dental and vision coverage. If health care costs increase more than expected, as determined by cost of an identified standard benefit option under the Federal Employees Health Benefits Program, then initial threshold will be automatically adjusted upwards. This provision also includes an adjustment for retirees ages 55-64 and for employees in high-risk jobs.