Medicare Basics

An Overview

You probably know that Medicare is a federal health insurance program for people 65 and older and others with certain disabilities. Now that you’re eligible or becoming eligible in the near future, it’s time to learn how Medicare works, what the different plans or parts are and how they fit into your current situation.

Medicare helps you get the coverage you need, but you should expect to pay some of the costs. If you choose Medicare Part A and Part B, you’ll find gaps in the coverage. Many people enroll in a Medicare Advantage, Part D Prescription Drug and/or a supplemental plan to help pay for the costs and benefits that aren’t covered by Original Medicare.

It’s easy to know if you’re eligible.

If you’re turning 65, you have an opportunity to enroll in a Medicare plan. You can enroll three months before the month you turn 65, the month of your birthday and three months after. If you wait to enroll in a plan, there is a chance you’ll have fewer plan choices, and you may have to pay more.

When are you eligible?

You are eligible for Medicare if:

If your health care needs change over time. So will the health plans you want to choose. You’re not locked into one plan permanently. You’ll have an opportunity to change plans at least once a year.

Here are some things to know about the “age 65” rule.

Who does the paperwork?

The Social Security Administration handles most of the paperwork for joining Medicare. The first letter you get in the mail about Medicare will probably come from Social Security. If you’re drawing Social Security benefits when you turn 65, Social Security will automatically enroll you in Medicare Part A and Part B.

Social Security can also help you find out if you’re eligible for extra help with the cost of Medicare coverage.

What happens to the health coverage I have now?

As you make your decisions about Medicare, keep your current health coverage in mind. This could be retiree health coverage from your former employer or your union, if you’ve retired.

If you’re still working, you may have health coverage from your current job. Or you may have purchased your own health insurance.

You’ll need to find out whether you can keep any coverage you currently have, and what your costs might be. You may have more choices available to you than the standard choices described in this guide.

Explore your options with someone who’s familiar with the details of the coverage you have now. If it’s coverage from an employer or a union, you can start with a human resources manager or a benefits specialist. Or talk to customer service at the insurance company that provides the plan. Do your research well. In some cases, if you keep your current coverage and wait until later to join Medicare, you may have fewer choices and pay more.

This content is republished with permission from medicaremadeclear.com

You probably know that Medicare is a federal health insurance program for people 65 and older and others with certain disabilities. Now that you’re eligible or becoming eligible in the near future, it’s time to learn how Medicare works, what the different plans or parts are and how they fit into your current situation.

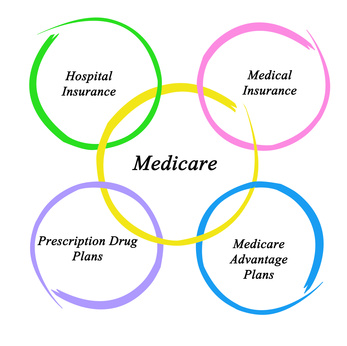

- Medicare Parts A and B are considered Original Medicare.

- Part A pays for hospital care, and Part B pays for doctor visits and outpatient care.

Medicare helps you get the coverage you need, but you should expect to pay some of the costs. If you choose Medicare Part A and Part B, you’ll find gaps in the coverage. Many people enroll in a Medicare Advantage, Part D Prescription Drug and/or a supplemental plan to help pay for the costs and benefits that aren’t covered by Original Medicare.

- Medicare Part C (Medicare Advantage plans) covers all the services that Parts A and B cover.

- Medicare Part D plans help with prescription drug costs.

- Medicare Supplement Insurance plans (Medigap) help cover some of the costs that Parts A and B don’t cover.

It’s easy to know if you’re eligible.

If you’re turning 65, you have an opportunity to enroll in a Medicare plan. You can enroll three months before the month you turn 65, the month of your birthday and three months after. If you wait to enroll in a plan, there is a chance you’ll have fewer plan choices, and you may have to pay more.

When are you eligible?

You are eligible for Medicare if:

- You’re 65 or older, or have a qualified disability.

- You’re a U.S. citizen or legal resident for five consecutive years.

If your health care needs change over time. So will the health plans you want to choose. You’re not locked into one plan permanently. You’ll have an opportunity to change plans at least once a year.

Here are some things to know about the “age 65” rule.

- Even if you’re already collecting Social Security, you must wait until you’re 65.

- You must be 65. Your spouse’s age doesn’t count.

- Even if you’re not collecting Social Security yet, you’re eligible at age 65.

Who does the paperwork?

The Social Security Administration handles most of the paperwork for joining Medicare. The first letter you get in the mail about Medicare will probably come from Social Security. If you’re drawing Social Security benefits when you turn 65, Social Security will automatically enroll you in Medicare Part A and Part B.

Social Security can also help you find out if you’re eligible for extra help with the cost of Medicare coverage.

What happens to the health coverage I have now?

As you make your decisions about Medicare, keep your current health coverage in mind. This could be retiree health coverage from your former employer or your union, if you’ve retired.

If you’re still working, you may have health coverage from your current job. Or you may have purchased your own health insurance.

You’ll need to find out whether you can keep any coverage you currently have, and what your costs might be. You may have more choices available to you than the standard choices described in this guide.

Explore your options with someone who’s familiar with the details of the coverage you have now. If it’s coverage from an employer or a union, you can start with a human resources manager or a benefits specialist. Or talk to customer service at the insurance company that provides the plan. Do your research well. In some cases, if you keep your current coverage and wait until later to join Medicare, you may have fewer choices and pay more.

This content is republished with permission from medicaremadeclear.com